Insatiable demand for protein has been a persistent trend over the past few years as TikTokers and other social media influencers tout its health benefits, and GLP-1 drug users are encouraged to follow a high-protein diet. With dairy viewed as a high-protein, low-calorie food, these patterns are impacting product mix and commodity pricing.

The cottage cheese category illustrates this trend. Last year’s production of lowfat and cream-style cottage cheese was the highest since 1988 after years of dwindling consumption. Processors are responding to the upswing in demand by adding capacity and updating facilities, which will require more protein and solids.

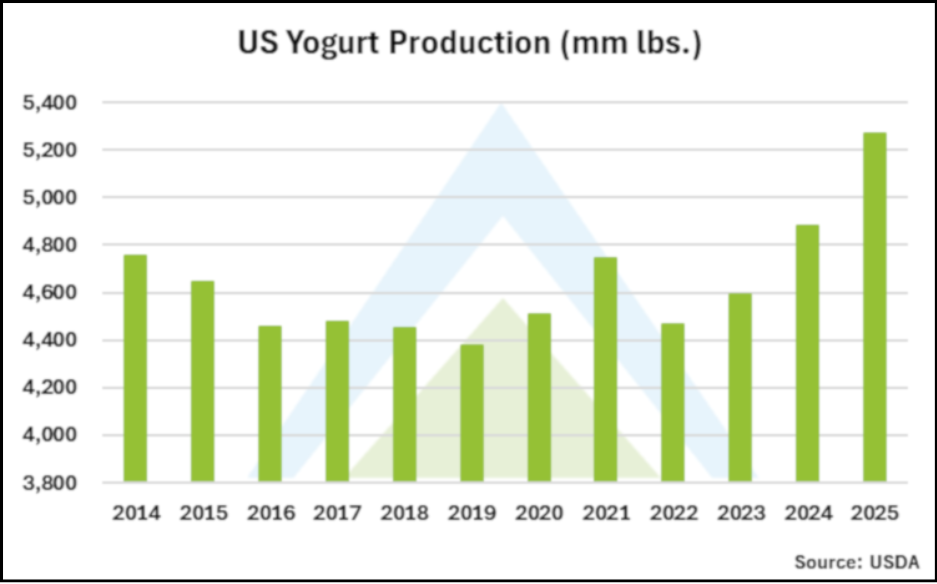

Yogurt production is also surging. Last year, U.S. output totaled 5.268 billion pounds, up 8.3% annually, demolishing the previous record set just a year earlier. Before this, peak yogurt occurred in 2014 during the Greek yogurt boom, highlighting just how big 2025’s production number was. Using USDA data, HighGround estimates that it took an additional 64 million pounds of skim solids to make this record level of yogurt. Dairy Management Inc. data show that 2025’s U.S. yogurt sales were roughly 53% Greek-style, 43% traditional and the remainder in other varieties. Regardless of type, yogurt is a high-protein, relatively low-calorie offering, making it an appealing choice for protein-conscious consumers.

Yogurt production is also surging. Last year, U.S. output totaled 5.268 billion pounds, up 8.3% annually, demolishing the previous record set just a year earlier. Before this, peak yogurt occurred in 2014 during the Greek yogurt boom, highlighting just how big 2025’s production number was. Using USDA data, HighGround estimates that it took an additional 64 million pounds of skim solids to make this record level of yogurt. Dairy Management Inc. data show that 2025’s U.S. yogurt sales were roughly 53% Greek-style, 43% traditional and the remainder in other varieties. Regardless of type, yogurt is a high-protein, relatively low-calorie offering, making it an appealing choice for protein-conscious consumers.

Ultrafiltered milk beverage consumption is also on the rise. These products contain milk that has undergone ultrafiltration, which removes lactose and water and concentrates the milk, resulting in a higher protein content. Although offerings were limited just a few years ago, more dairy cooperatives and manufacturers are making this a retail product, increasing competition and purchases. Ultrafiltered milk is also produced for use in cheese vats, providing a secondary use and a greater pull on skim solids.

Cheese and whey also require skim solids, particularly protein, for their production. HighGround estimates, based on 2025’s USDA data, that the 3.2% annual uptick in cheese production resulted in an additional 150 million pounds of skim solids pulled, and about 40 million pounds for whey protein concentrate 80 and whey protein isolate.

This increase in Class II product production, along with the strong draw of ultrafiltered milk and the new cheese capacity in the Central U.S., has tightened the availability of skim solids. Nonfat dry milk (NDM) and skim milk powder (SMP) dryers have been most impacted. Combined totals for these commodities in January hit their lowest volume for the month since 2015. With more milk being shunted away from dryers toward higher-end, value-added products, NDM/SMP prices have increased considerably.

This increase in Class II product production, along with the strong draw of ultrafiltered milk and the new cheese capacity in the Central U.S., has tightened the availability of skim solids. Nonfat dry milk (NDM) and skim milk powder (SMP) dryers have been most impacted. Combined totals for these commodities in January hit their lowest volume for the month since 2015. With more milk being shunted away from dryers toward higher-end, value-added products, NDM/SMP prices have increased considerably.

However, domestic dynamics are not the only pain point in the skim-solids balance sheet. Geopolitical tensions have caused buyers to fill more than short-term needs and secure long-term supplies, another factor behind higher NDM/SMP prices in 2026. The latest hot spot is the war in Iran and the de facto closure of the Strait of Hormuz, a major maritime transit lane for energy and freight. This blockade of the strait means shipping routes to the Middle East and North Africa will change, and commodity price volatility is expected to increase. Food security is also an issue as the region imports 80%-90% of its food, according to Reuters.

For dairy, the closure may cause exports destined for the region and beyond to back up, driving prices lower as dairy exporters seek homes outside the region. Lengthier routes may also add costs to dairy commodities, tempering demand. Further, inflationary pressures are expected to rise if the conflict persists, potentially reducing consumer spending and negatively affecting dairy demand. On the other hand, buyers may continue their relentless purchasing to ensure that food security will not be an issue during wartime.

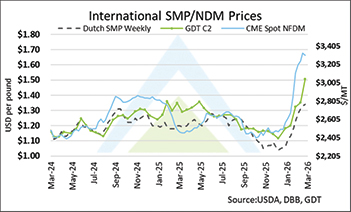

For now, the impact of the change in product mix and nervousness is being reflected in NDM and SMP prices. Dutch SMP prices are up 29% since late December, at $2,952 per metric ton (MT) as of March 7 ($1.34 per pound). At the Global Dairy Trade auction, the New Zealand-sourced Fonterra C2 contract (May delivery) has soared to its highest price in over three years, up 34% since the end of 2025, settling at $3,320/MT ($1.51 per pound) at the first March auction. And U.S. prices have led the charge, rising as high as $1.7225 per pound (March 11), a 47% gain since the start of 2026.

While global milk supplies remain robust and U.S. protein test within the milk continues improving, strong demand and a desire to lock in future supplies have fueled a significant NDM rally. This trend is unlikely to persist beyond the first half of 2026, but strained relations could keep buyers active.

Reprinted with permission from the March 13, 2026, edition of CHEESE MARKET NEWS®; © Copyright 2026 Quarne Publishing LLC; (608) 288-9090; www.cheesemarketnews.com