In mid-March 2026, one of China’s largest nutritional supplement companies made headlines in the trade press. BYHEALTH – a Guangzhou-based brand that has sold protein powder in China for 30 years and counts protein as one of its core franchise products – announced an upgrade to its flagship protein powder, raising the protein content from 80% to 90% and incorporating imported New Zealand whey protein isolate (WPI) as a key ingredient. The launch was showcased at the Bo’ao Food for Health Science Conference in Hainan, and in the same breath, the company announced its first entry into Food for Special Medical Purposes (FSMP) – a regulated category covering clinical and post-surgical nutrition – using whey protein concentrate (WPC) as the base ingredient.

It is a small product launch from a single company. But it is also a window into something much larger: a structural shift in how Chinese consumers think about and consume dairy that has been quietly reshaping China’s dairy import mix for the better part of five years.

A growing body of research in China is drawing direct links between diet and mental health outcomes — and dairy keeps showing up on the right side of that equation. A Shandong University study found that a vegetable–egg–beans–milk dietary pattern was associated with a lower risk of depression among adults aged 60 and above. Innova Market Insights notes that Chinese consumers explicitly associate dairy with comfort, positioning it alongside fruit as a category associated with emotional well-being. Thirty percent of Gen Z and millennial consumers in China report worrying about their mental health, and fresh, natural foods — dairy prominently among them — are increasingly where they turn first. That this research was largely completed around 2021 makes it all the more important as context for what the import data has been showing ever since.

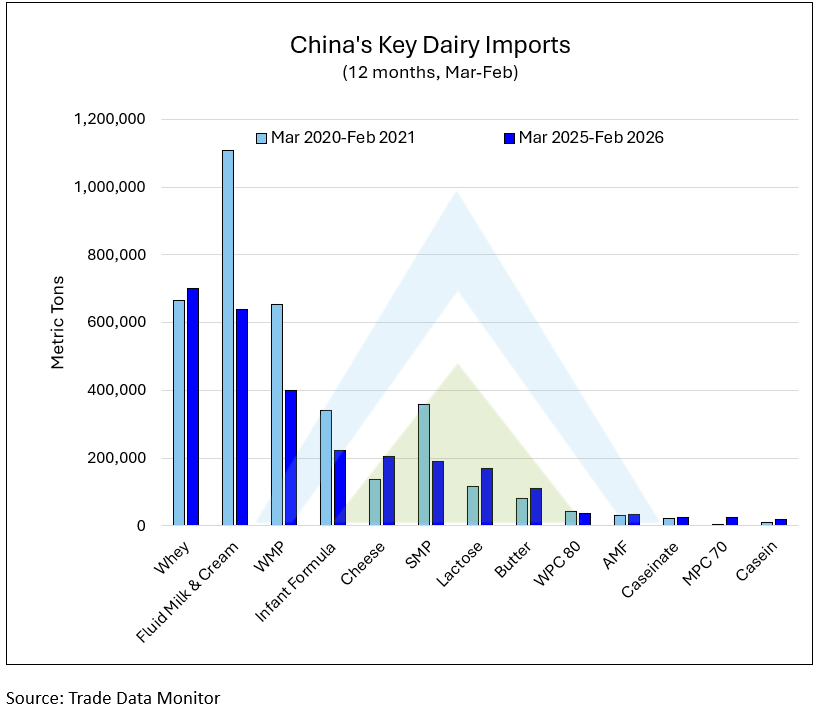

Total Chinese dairy imports for the 12 months ending February 2026 came in at 2.78 million MT – down 22% from the 3.57 million MT recorded in the comparable period five years prior. But that decline masks a significant rotation in what China is actually buying. (HS Codes included in total import figure: 040410, 0401, 040221,190110, 0406, 040210, 170211, 170219, 040510, 350220, 040590, 350190, 040490, 350110)

Whey is the standout, and at 701,000MT for the 12 months ending February 2026, it is now the single largest dairy import category by volume – up 5.5% over five years, even as the overall import basket contracts. That combination – flat-to-growing volume in a shrinking market – means whey is actively taking share. A large portion of China’s whey imports are low-protein feed-grade product, primarily sourced from the US and used in pig and poultry nutrition, but food-grade products are also in the mix. Another telling signal is in the functional tiers: WPC 80+ has been relatively flat despite prices at historic highs, and MPC and natural milk concentrates are up 539% over five years – a solid signal in the data that China’s demand for high-functionality dairy proteins is accelerating.

Cheese and Butter: The Foodservice Half of the Story

Cheese at 205,700MT for the 12 months ending February 2026 – up 50% over five years and still running at +17% year-over-year – is the fastest-growing major import category during that timeframe. This is a B2B and foodservice phenomenon, driven by mozzarella for pizza chains, processed slices for burger and sandwich formats, and cream cheese for the milk tea and café sector. Butter is up 38% over the same period to 111,200MT, with strength coming from baking and foodservice expansions. Lactose has also shown significant growth, up 68% to 168,800MT, likely reflecting demand for infant formula reformulation, skim milk powder (SMP) fortification, and growth in nutraceutical manufacturing.

The Powder Collapse Is Structural, Not Cyclical

The other side of the trade data rotation, SMP, WMP, and fluid milk, is clearly DOWN. SMP imports have fallen 47% over five years to 191,000MT. WMP is down 39% to 399,000MT. Fluid milk imports declined 42% to 639,900 MT. These should not be confused with cyclical fluctuations tied to price or exchange rate movements, as they reflect a fundamental change in how China sources and consumes dairy.

Further, the shelf-stable fluid milk model is being displaced on both the supply and demand sides. Domestic production has scaled to cover standard powder needs, and Chinese consumers are increasingly choosing fresh, pasteurized milk supplied through local cold chains over reconstituted UHT products. The revised national sterilized-milk standard has reduced the use of powder-based reconstitution in UHT milk formulations.

What BYHEALTH Tells Us About the Consumer Side

The trade data shows what China is importing. The BYHEALTH launch is an example that shows why. Protein supplementation in China is moving from a niche category associated with bodybuilding and elite sports nutrition into a mainstream health purchase. BYHEALTH’s deputy director of nutrition research cited three distinct consumer segments driving demand: fitness enthusiasts seeking higher-quality protein, consumers on a weight management journey facing insufficient protein intake, and an aging population with clinical nutritional needs.

China designated 2024–2026 as the Years of Weight Management, making it a formal policy priority. The country saw roughly 100 marathons per weekend in April and May of 2025 alone – a figure that has prompted dairy brands like Mengniu to expand their sports nutrition ranges. GLP-1 adoption is also growing in China, and while penetration remains lower than in Western markets, the drug’s well-documented effect of accelerating muscle loss is driving a parallel conversation about protein adequacy that plays directly into premium supplement demand. In the FSMP category, protein powder is already the most common product type sold to elderly consumers on China’s largest e-commerce platforms, according to Alibaba Tmall.

The Zhenzuan upgrade to 90% protein content, using New Zealand-sourced WPI in a 2:3 animal-to-plant protein ratio, is a direct product response to that consumer shift.

Implications for Global Dairy Trade

For exporters and producers tracking China’s demand, the message in this data is consistent with what HighGround Dairy has been observing across global dairy markets – the premium protein supply chain is tightening, and China will be a key contributor on the demand side.

Functional ingredient capacity is expanding across New Zealand, Ireland, the United States, and Denmark – but demand is outpacing new supply. New Zealand sits at the center of this, both as a direct WPI exporter to China and as the preferred whey origin for Chinese supplement brands like BYHEALTH.

The broader takeaway: China’s dairy import story is no longer primarily about volume in standard commodities. It is increasingly about value in functional ingredients – proteins that perform, fats that serve a purpose, and formats that fit how Chinese consumers eat and live today. Although, given China’s continued focus on domestic expansion and industry support, it is hard to see a path where the country does not accelerate investment in its own high-protein capabilities.

Read more about China’s trade volumes in the January & February 2026 China Dairy Import Volume Analysis, including HighGround Dairy’s opinion. Not a subscriber yet? Click here to sign up for a free trial to read the entire report today.