USDA released its semi-annual Cattle Inventory report on January 31st with the total of all cattle, including calves, summing to slightly less than 87.2 million head, down 2% from the Jan 1, 2023 figure. This is the fifth consecutive year-on-year decrease and the lowest number since the 1951 survey. However, this was mainly driven by the shrinking beef herd, which has dealt with ongoing drought for several years, limiting rangeland and grazing capabilities. High feed costs in past years have not helped either.

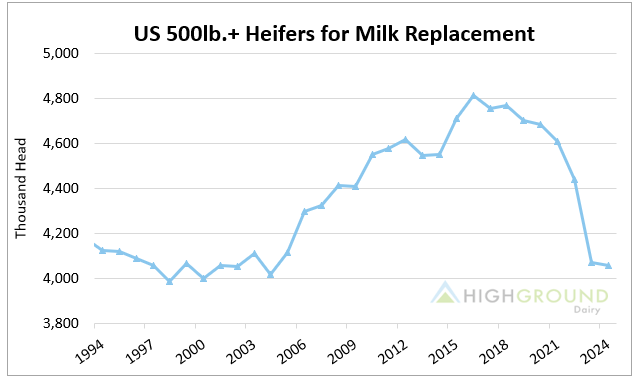

In the dairy cattle space, 9,356,800 head were counted in the US at the first of the year, declining just 0.4% from the prior year. Heifers for milk cow replacements (500 lb. or greater), the highly anticipated number in the report, totaled 4.059 million head, falling 0.4% year-over-year.

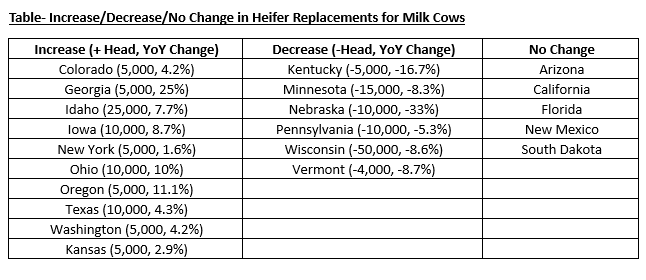

However, the bigger story was in the Jan 1, 2023 estimate revision. USDA significantly lowered the initial print of 4,337,200, decreasing it by 263,600 head – a sizable 6.5% downward revision! Jan 1, 2024’s heifer numbers are the lowest data point since 2004. It is important to note that the total US milking herd counted to 8,987,500 then, meaning that on a percentage basis, the ratio of heifers to milk cows was 44.7%, compared to 43.4% in 2024. The smaller heifer-to-cow ratio is evidence supporting a smaller milking herd in 2024 and higher replacement prices. Breaking the replacement heifer data down to a state level shows some places increased heifer inventories, e.g., Idaho, while others, such as Wisconsin, saw significant declines. Some of the losses in the Upper Midwest may be due to more producers shipping heifers to custom raisers in the Southwestern US.

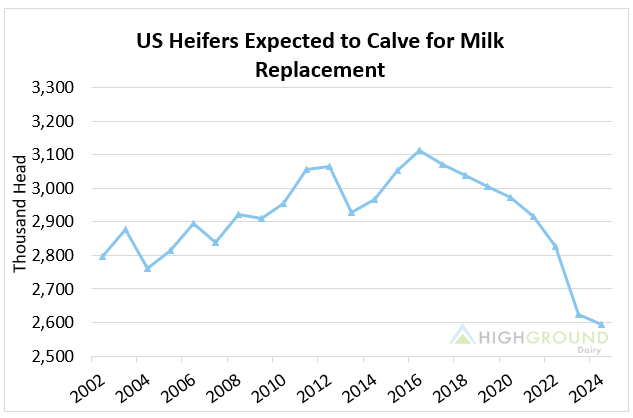

When looking at heifers expected to calve, USDA calculated 2,593,400 animals, the lowest number since this data set began in 2002. Comparing heifers to calve to the number of cows, yields a restock rate of 27.7%, also the smallest value since 2002. Last year’s and 2022’s rates are the next smallest in the set, sitting at 27.9% and 30.1%, highlighting that the heifer inventory issue began before 2024.

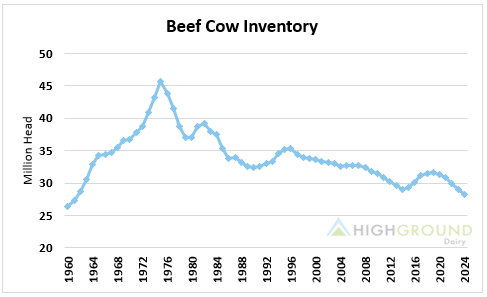

Beef cow numbers matter too, and those dropped by 2.4% year-on-year, meaning the beef herd is not in recovery mode yet either. Jan 1, 2024’s total of 28,223,000 logged the smallest number since 1961.

Corroborating with the dismal size of the beef cow herd was a small calf crop in 2023 that reached 33.592 million, the lowest since 2014. Even more notable, 2023’s calf crop was the second lowest point in the survey data going back to 1977. The situation does not appear it will remedy itself soon, either, as beef replacement heifers of 4,858,300 head declined by 1% from 2023, and USDA revised Jan 1, 2023’s figure lower by 234,100 head, or -4.7% of the total. Beef heifers expected to calve decreased by the same 1%, and the 2023 total was changed by 58,500 head.

All this is to say that without cows and heifers to birth more steers and increase beef supplies, dairy will remain a worthy substitute. Dairy farmers in 2023 took advantage of these record-high values, culling cows heavily through the beginning of September to combat low on-farm margins before slowing the last few months of the year and plummeting at the start of 2024. Continued tight beef supplies will keep prices elevated and may make it very tempting for farmers to cull if on-farm margins get low enough. Further, heifer prices are already rapidly increasing, and with the winnowed inventories, they will likely only move higher. With total steers of 15,789,200 as of Jan 1, 2024 (-2% YoY), the smallest since 2015, this supports the thesis that fewer cows means fewer babies, creating low supplies and keeping high prices. As drought persists, the plight of ranchers will continue, and it will take some time before the beef herd recovers, meaning the trend of competition for dairy cows and heifers for the beef market will also continue.