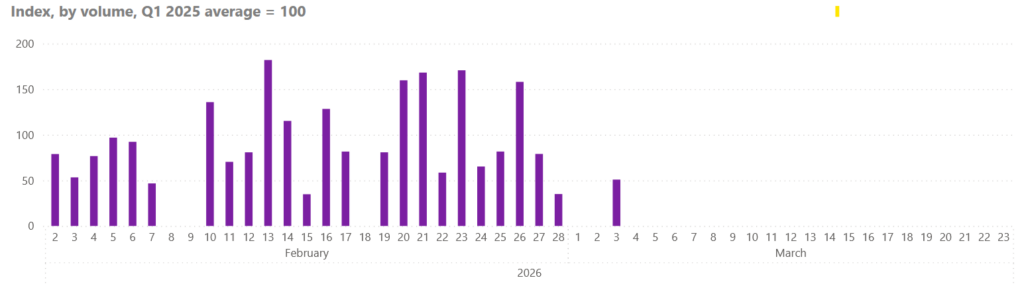

Fertilizer costs are soaring just weeks before planting is set to begin in the US. Some farmers locked in fertilizer prices last fall, but those who did not are now facing steep cost increases driven by the conflict involving Iran and disruptions in the Strait of Hormuz. The waterway is a critical artery for global energy and fertilizer shipments. One-third of the global seaborne fertilizer trade passes through the Strait, while an estimated 20% of the world’s oil passes through the passageway, including liquefied natural gas, an important feedstock for nitrogen-based fertilizers. (See Figure 1)

Figure 1: Fertilizer-related Outbound Shipments Through the Strait of Hormuz (AIS-Traceable Vessels Only), Source: WTO

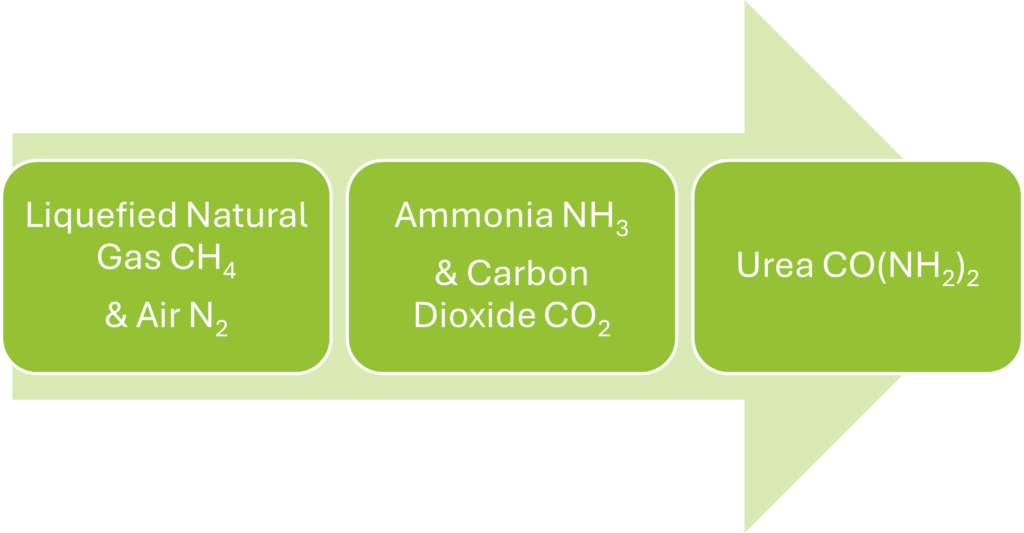

Nitrogen is the most commonly used fertilizer in the world, accounting for 59% of global use, followed by phosphate at 21%, and potassium at 20%. Natural gas is used to make ammonia, which can then be used to produce urea (Figure 2). Of the fertilizers exported from the region, urea, the most commonly used nitrogen-based fertilizer, is the most affected, with about 30-35% of the world’s exports moving through the shipping lane. Ammonia, another nitrogen-based input, is also affected. Beyond finished fertilizer trade flows, disruptions to natural gas, particularly LNG, are compounding the issue upstream. The LNG stoppage is already creating operational challenges, with the Carnegie Endowment for International Peace reporting that nitrogen fertilizer producers in Pakistan, India, and Bangladesh have halted operations due to the Hormuz shutdown.

Figure 2: Production of Nitrogen-Based Fertilizer Products

Phosphorus fertilizers are similarly exposed. Roughly 20% of global phosphate fertilizers, including DAP (diammonium phosphate) and MAP (monoammonium phosphate), transit through the strait. At the same time, Gulf exports of sulfur — a critical feedstock for downstream phosphate production — are being constrained, forcing converters to slow output.

These combined disruptions across both nitrogen and phosphate supply chains are now showing up clearly in pricing. Since the war’s onset, fertilizer prices have surged. For example, the March 2026 Urea (Granular) FOB US Gulf futures contract was at $465.50/MT on February 27, the day before the war began, and has since climbed to $621/MT as of March 23 — a 33% increase in less than a month (Figure 3).

Figure 3: March 2026 CME Urea Futures Contract (FOB Gulf), Source QST

The 2026–27 crop season was already under pressure for US farmers, following a financially poor 2025–26 season. CME corn futures through March 2027 are all below $5/bu., and soybean contracts remain below $12/bu., levels that are not particularly supportive. Rising input costs will push margins even deeper into the red.

Further, the impact on the global supply chain will continue to drive up stateside prices for energy and fertilizers. History shows that rising oil prices eventually lead to higher food costs, so while consumers are currently feeling the pain at the gas pump and at the ag cooperative, the pinch at the grocery store may follow in the coming months. Higher diesel prices are adding another layer of pressure by increasing the costs of fieldwork, transportation, and fertilizer application during an already tight planting window.

For US producers, corn requires more fertilizer than crops like soybeans. With this crisis occurring so close to peak planting, farmers may adjust crop plans, planting more soybeans, which are less fertilizer-intensive, and less corn. All eyes will be on the USDA’s Prospective Plantings report next week, March 31, to see how much plans have shifted for the 2026–27 growing season.

Just as concerning is the impact on other nations that are even more reliant than the US on Middle Eastern fertilizers. United Nations analysis indicates that among the top five importers of Persian Gulf fertilizers, three — Sudan, the United Republic of Tanzania, and Somalia — are among the least developed countries in the world, with Sri Lanka also in the mix as a developing economy. Rising input costs in these regions threaten food security and could lead to increased hunger.

The geopolitical situation remains fluid. As of Monday, March 23, President Trump announced he would hold off on attacking Iran’s power plants — a threat made over the weekend — for five days following what he described as productive talks. Iran has denied any such progress. Oil prices have eased, and equity markets have moved higher on the announcement, relieving some pressure. That said, it remains unclear whether further progress can be made, and global concerns around oil, fertilizer, and food prices persist. Until the conflict reaches a meaningful resolution and the Strait reopens, these supply chains remain vulnerable.