The Commitment of Traders (COT) report is a weekly publication by the Commodity Futures Trading Commission (CFTC) that provides information on the positions held by various market participants, such as commercial hedgers, non-commercial speculators, and small traders, in futures markets. It is widely followed by traders and analysts to gain insights into market sentiment and potential price movements.

The COT report categorizes market participants into the following reporting bodies:

- Commercial Traders (Hedgers): These are businesses involved in the production, processing, or distribution of physical commodities or financial instruments. They use futures and options markets to hedge against price risk related to their underlying assets.

- Non-Commercial Traders (mostly speculators): This category includes large institutional investors, such as hedge funds and investment funds, who trade in the futures market for speculative purposes rather than to hedge against physical positions.

- Swap Dealers: These institutions include banks, investment banks, and other financial intermediaries.

- Managed Money: Large institutional investors, such as hedge funds, commodity trading advisors (CTAs), and other investment funds.

- Other Reportables: Asset Managers, Leveraged Funds, liquidity providers, individual traders

- Non-Reportable Traders (Small Traders): These are traders that carry smaller positions in the futures market. Their positions are below the reporting threshold set by the Commodity Futures Trading Commission (CFTC) and, therefore, not broken down by specific trader category.

The analysis of futures & options positions held by the different market participant groups provide valuable insights into their trading behavior, contributing to a deeper understanding of overall market dynamics and potential price trends.

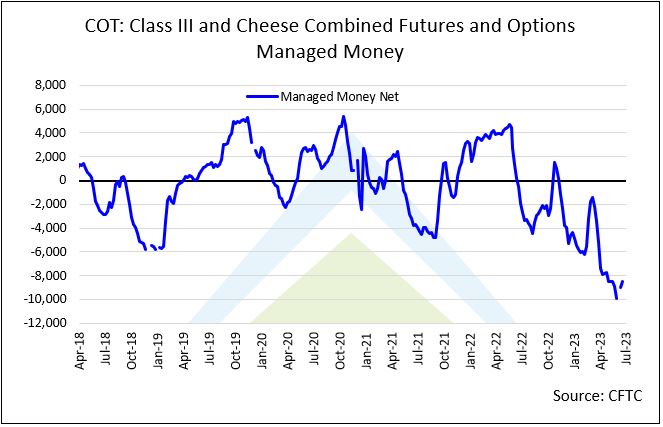

A notable observation in dairy markets is that commercials have been maintaining and growing a strong net long position in response to prices that have moved lower, making them more attractive to own, even with increased availability of excess milk and commodities during the second quarter. The recent data in the Class III vs. CSC Cheese breakdown has revealed some interesting trends. Historically, Class III commercials were usually net short, while cheese hedgers tend to be net long. However, due to the significant decline in Class III prices, even Class III hedgers are now net long, indicating a notable shift in market dynamics. However, the most compelling aspect of the data lies with Managed Money position, which has consistently maintained a net short position for 32 consecutive weeks.

As recent as the June 27th report, Managed Money traders had established a record short position (-9,876 positions) in Class III Milk and Cash Settled Cheese (combined futures and options). Although there has been a slight reduction in this net short position with the recent price rally, as of July 18, Managed Money remains significantly short.

Now as fundamentals lean less bearish throughout Q3 and into the end of the year, with US milk production turning negative early in last week’s report, speculative traders continue to reduce their short position in the dairy markets, which now sits at -2,603 within Cash-Settled Cheese (2nd highest managed money net short position on record) and -5,874 in Class III Milk (8th highest net short position on record).

This juxtaposition of positions between Managed Money and commercials has played a role in keeping prices subdued over the past few months. This data raises questions whether Managed Money will continue to hold these positions during the recent market rally. While the data suggests that they have for the most part, the possibility of that group of traders unwinding, or buying back, a significant portion of their positions could contribute to further fueling the current rally, at least in the short term. The market dynamics remain closely monitored, and traders are observing these developments to gain insights into potential price movements.