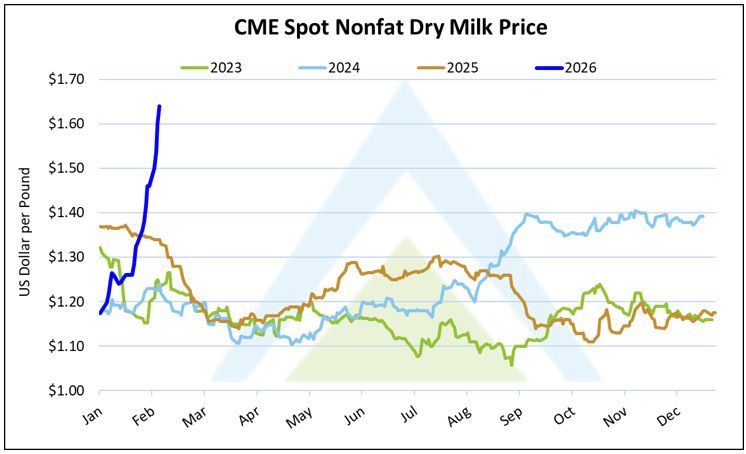

For nearly everyone in the dairy industry right now, there is confusion, a bit of shock, and a lot of questions. The scale and speed of the recent move in nonfat dry milk has been difficult to process in real time, particularly given the confidence around abundant supply assumptions entering the year. CME spot nonfat dry milk opened 2026 at $1.1750/lb. and has since surged to $1.60/lb., a gain of nearly 40% in just a matter of weeks. On the CME futures side, March ’26 NFDM bottomed near $1.09/lb. and traded as high as $1.5755/lb., representing a rally of more than 44% from the lows.

Spillover support into other markets has also become visible, particularly on butter. CME spot butter traded as low as $1.30/lb. as late as January 13 and just 3 ½ weeks later (18 trading sessions), rallied to roughly $1.71/lb., nearly a 32% gain. As a result, the CME Class IV complex has traded on expanded limits for nine sessions since January 22, pushing volatility to levels not seen since the unprecedented supply chain disruption during COVID-19 in Q2 2020.

Between sharply higher year-on-year milk production growth in the US, Europe and New Zealand along with a persistent lack of demand urgency, industry participants close to day-to-day market conditions leaned decisively bearish. It helped that NFDM prices spent all of 2025 confined to a roughly 25-cent range with very little volatility, dulling sensitivity to how fragile the underlying balance sheet had become.

In 2023, the US produced 2.5 billion lbs of combined NFDM and skim milk powder. By 2025, output had fallen to 2.1 billion lbs, a loss of 412 million pounds, or roughly 16%, in just two years. The decline was driven by weaker demand, but it left the balance sheet tighter than normal. As long as buyers remained patient, hand-to-mouth, with a sluggish tone, that tighter structure felt manageable. But when the product mix continues to shift, headline risk tells buyers and traders to cover their shorts setting off a short term demand surge and a supply-side hiccup occurs, that was all that was needed to ignite the powder keg in the NFDM market.

What started as modest support in Q4 2025 tied to tightness in the Upper Midwest escalated rapidly given that Class II demand remained firm (think yogurt, cottage cheese, high protein milk beverages) continuing to pull on skim solids in that region. In 2025, cottage cheese production rose to levels not seen since 1989 with a year-on-year gain of nearly 10%. Yogurt production was also at record highs in 2025, UP 7.9% over 2024. When Midwest processors began to feel the strain, buyers still assumed the West Coast would make up any shortfalls. Instead, production delays emerged in that region, kicking off a physical squeeze that has not been seen in years…

Layered on top of this short-term domestic tightness is an intensifying global pull. Recent Global Dairy Trade events have featured strong SMP bidding as buyers work to pad supplies amid geopolitical uncertainty. More importantly, renewed concerns around infant formula (IF) supply have added fuel to the fire as well. On Thursday, February 5, Danone announced a broader IF recall in Europe, following earlier recalls over the past two months that also involved Lactalis and Nestlé, reigniting efforts to rebuild inventories across Europe. While dairy is not the source of the recall (linked to arachidonic acid (ARA) oil, an infant formula ingredient), rebuilding supply could increase usage of milk powders in the short term.

HighGround’s Take: Our broader supply/demand view has not materially changed, though the squeeze is real and will still take some time to sort itself out, so volatility will continue throughout February. NFDM remains a secondary protein outlet over the long term, whey protein continues to be the preferred destination for milk solids, and overall milk supply remains ample. In fact, the recent rally only gives farmers around the world more incentive to lock in very good profits through the remainder of 2026. As a result, HighGround will likely be extending milk production growth forecasts – more milk for longer. While $1.05/lb. NFDM is likely off the table in 2026 given this recent rally, $1.60/lb. is an extremely overbought level that will not last another month before the Northern Hemisphere flush cools prices significantly in Q2.