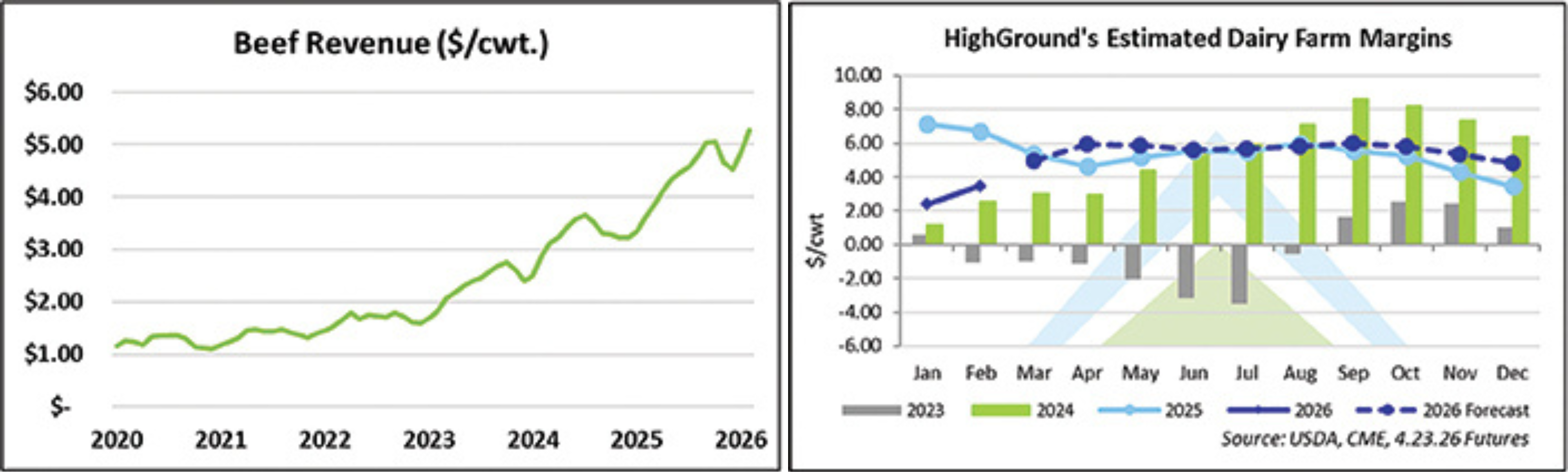

HighGround Dairy’s model indicates that on-farm producer margins are poised to remain in the black for the remainder of 2026. The calculation includes milk revenue based on Class III and IV pricing and average component levels, revenue from crossbred calves and cull cows, feed costs using corn and soybean meal futures, and fixed feed and non-feed costs. While nothing is certain, one revenue source seems likely to remain robust in 2026: beef. Over the past few years, beef revenue — i.e., cull cows and bull calf sales — has skyrocketed for dairies due to strong feeder and live cattle futures prices.

Our model forecasts that in 2021, revenue from these sales generated an additional $1.37 per hundredweight, but grew to $4.40 per hundredweight in 2025, an increase of over 200%. Thus far in 2026, with just two months in the books, our estimates show that total income is over $5 per hundredweight and poised to push higher in the coming months.

The excitement in the cattle markets seems almost too good to be true. While record-high cattle prices will not persist forever, there are reasons to remain bullish and expect prices to remain above five-year averages for at least the next few years if market conditions remain the same. The first is the extremely small U.S. beef herd, which is at its lowest level in 75 years, according to the most recent USDA Cattle Inventory report. Beef cows, a subset of the overall number, totaled 27.6 million head in January, the smallest since 1961. Another reason is the ban on cattle imports from Mexico due to New World screwworm, which adds pressure to tight supplies. With a 18- to 24-month production cycle for a steer, and a limited number of cows, rebuilding the herd will take time.

Weather adds another constraint. As of April 21, 63% of the cattle inventory was in a drought-affected area. Past droughts hit the Southern U.S. grazing lands, and the beef herd decreased. Heifers and cows were sent to slaughter, reducing breeding stock and creating a bottleneck. If drought occurs, this will provide support to cattle prices.

As protein grows in popularity and on-shelf prices rise, consumers have remained resilient, continuing to buy beef. Prices may rise as grilling season begins and demand seasonally increases. Strong demand for all things protein is bullish for cattle prices.

Downside risks remain. However, for all the reasons listed above, a surge in cattle inventories is unlikely, meaning demand would have to decline drastically. Consumer sentiment is currently at an all-time low, according to the University of Michigan sentiment survey. Other data from the Surveys of Consumers at the University indicate that Americans are concerned about the job market and inflation and are reducing their spending accordingly. This is particularly noticeable in the foodservice sector, where value offerings and promotional deals dominate the landscape. Fast-food and casual-dining brands have been leaning into chicken lately as beef prices soar, but this does not mean Americans’ taste for beef has diminished. Current events, animal disease and macroeconomic news are worth monitoring to assess their impact on cattle prices.

On top of hearty beef prices, milk revenue has also increased since the start of 2025, and feed costs are reasonable. As of April 22, Class IV futures for April to December 2026 have increased by nearly $5 per hundredweight from just three months ago. Soaring nonfat dry milk (NDM) prices have provided the lift, and this increase bodes well for producers in Class IV-heavy regions. Further, while not as large, April to December 2026 Class III futures are up over $1 per hundredweight since Jan. 23, also adding support. Corn and soybean meal prices have declined slightly over the last month, and alfalfa hay prices are below the five-year average.

Even with January and February’s sub-$3 per hundredweight margins included in our model, 2026 finances are penciling out to average $5.13 per hundredweight, based on April 23 futures. Much of this profitability is driven by beef revenue, which averages $5.09 per hundredweight, accounting for nearly all of it. Increased milk prices have lifted the annual average to $20.62 per hundredweight However, this is nearly offset by feed and fixed costs of $20.58 per hundredweight.

It is important to note that cattle or milk prices would need to decline steeply, or feed costs would need to accelerate rapidly, to push margins into the red. However, this forecast paints a clear picture of dairy farm profitability. Without beef sales, many dairy farmers would be struggling. In addition, our model is intended to represent an average dairy that purchases feed, which may vary by size, location or market, meaning some producers may be feeling a much greater pinch than these numbers indicate.

While the run-up in NDM prices has lifted milk revenue, it is unclear if these record prices will persist. Global milk production among the top five export markets has grown more than 4% over the past six months. This has not occurred since 2014, when quotas ended in Europe and New Zealand recovered from the 2012-13 drought.

Although geopolitical tensions and tightness in the U.S. NDM market have spurred higher prices, it seems unlikely to continue much more than a few months. While a global price downturn seems plausible, particularly in the second half of this year, milk in the U.S. may continue to grow, albeit at a slower pace, as total on-farm margins, driven by beef income, remain in the black for the largest farms.

Reprinted with permission from the May 1, 2026, edition of CHEESE MARKET NEWS®; © Copyright 2026 Quarne Publishing LLC; (608) 288-9090; www.cheesemarketnews.com